As On: Aug-11-2026 | 09:25 PM

INDU: FY26 EPS expected at PKR 333; 4Q at PKR 85.7, DPS at PKR 51

Published August 11, 2026

INDU is expected to announce its FY26 results, where we expect the company to report an EPS of PKR 85.7 in 4QFY26, up 4% YoY. This will take FY26 EPS to PKR 332.5, up 14% YoY. The company is also expected to announce a final cash dividend of PKR 51/share taking full year payout to PKR199/share.

FCCL: 4QFY26 EPS clocks in at PKR 2.2, up 38% YoY

Published August 11, 2026

FCCL announced its 4QFY26 results today wherein the company reported an EPS of PKR 2.20, up 38 % YoY. This takes cumulative earnings for FY26 to PKR 6.60/share, up 21% YoY.

FCCL: 4QFY26 EPS expected to clock-in at 1.98, up 24%, YoY

Published August 10, 2026

FCCL is expected to announce its 4QFY26 results, wherein we expect the company to report an EPS of PKR 1.98, up 24% YoY, taking FY26 EPS to PKR 6.37 (up 17% YoY). We expect the company to also declare a dividend of PKR 1/share for the full year.

KSE-100 INDEX: Rebound Tests Resistance (Technical Weekly)

Published August 10, 2026

KSE-100 Index extended its rebound, holding above the 50-day SMA (176,990) and rising trendline, keeping the short-term structure constructive...

Domestic Cement Demand Maintains Momentum, up 17% YoY in Jul-26

Published August 5, 2026

Pakistan’s domestic cement dispatches stood at 3.78mn tons, up 17% YoY in Jul-26, marking a strong start to FY27. This increase was a result of positive budgetary measures announced in FY27 budget for the real estate and construction sectors (including removal of Section 7E and reduction isn withholding taxes on property transfer), thereby leading to improved sentiment and construction activity. To recall, domestic dispatches rebounded 9.5% YoY in FY26 after four consecutive years of decline.

KSE-100 INDEX: Rebound Faces Resistance (Technical Weekly)

Published August 3, 2026

KSE-100 Index posted a weekly gap-up after three consecutive weekly declines, holding above the rising 50-week SMA (168,346), while the broader uptrend from June 2023 remains intact...

MLCF: 4QFY26 Consolidated EPS clocks in at PKR 4.07, up 17% YoY

Published July 31, 2026

MLCF announced its 4QFY26 results, wherein the company reported a consolidated EPS of PKR 4.07, up 17% YoY. This takes FY26 consolidated earnings to PKR 11.34/share, up 3% YoY. In line with the prevailing trend, the company declared no dividend for 4QFY26, resulting in a nil dividend payout for FY26.

Economy: Jul-26 Inflation Expected at 9.5% YoY

Published July 30, 2026

The National Consumer Price Index (NCPI) is projected to increase by 9.5% YoY in Jul-26, primarily reflecting base effect rather than a meaningful moderation in underlying inflationary pressures. On a month on month basis, inflation is estimated to rise by 1.5%, largely driven by higher food prices.

HCAR: 1QMY27 EPS clocked in at PKR 17.41, up 200% YoY, boosted by a one-off gain

Published July 29, 2026

HCAR announced its 1QMY27 results, reporting an EPS of PKR 17.41, up 200% YoY and 147% QoQ. The sharp jump was largely driven by a one-off, non-cash gain amounting to PKR 1.59bn that came from discounting of a future liability. Excluding this one-off, recurring EPS clocked in at PKR 6.3, broadly in line with our estimates. The company did not announce any cash dividend.

PIOC: 4QFY26 EPS clocks in at PKR 9.68, up 95% YoY

Published July 29, 2026

PIOC announced its 4QFY26 results today wherein the company reported an EPS of PKR 9.68, up 95% YoY. This takes cumulative earnings for FY26 to PKR 29.03/share, up 35% YoY. In line with the prevailing trend during the year, the company declared no dividend for 4QFY26, resulting in a nil dividend payout for FY26 (compared to DPS of PKR 10 in FY25).

HCAR: 1QMY27 EPS expected to clock in at PKR 6.29, up 9% YoY

Published July 28, 2026

HCAR is expected to announce its 1QMY27 results, where we expect the company to report an EPS of PKR 6.29 in 1QMY27, up 9% YoY (down 11% QoQ). We do not expect any cash dividend to be announced alongside the first quarter result.

Economy: SBP Holds Policy Rate Steady at 11.5%

Published July 27, 2026

The State Bank of Pakistan (SBP) kept the policy rate unchanged at 11.5%, reflecting its view that the current stance remains appropriate to guide inflation towards the 5-7% medium-term target range. The MPC assessed that the macroeconomic outlook has improved since the previous meeting though it remains susceptible to risks, particularly following the resurgence of conflict in the Middle East. The earlier de-escalation had eased global oil prices and supply chain disruptions supporting some improvement in recent economic indicators.

Cement Universe to Post Earnings of PKR 14.5bn in 4QFY26, up 13% YoY On Deferred Tax Liability Adjustment

Published July 27, 2026

Akseer’s Cement Universe is expected to report 4QFY26 earnings of PKR 14.5bn (+13% YoY), primarily driven by a one-off gain from the revaluation of deferred tax liabilities following the reduction in the super tax rate.

KSE-100 INDEX: Trendline Under Pressure (Technical Weekly)

Published July 27, 2026

KSE-100 Index extended its corrective phase, closing below the gap support at 173,093 and the rising 30-week SMA (172,073), reflecting further deterioration in near-term momentum...

KSE-100 INDEX: Gap Support Under Test (Technical Weekly)

Published July 20, 2026

KSE-100 Index moved in line with our previous view, extending last week's bearish follow through with a gap down opening after the Dark Cloud Cover candlestick pattern while testing the unfilled June 08 gap at 173,100...

20260713095627.png)

KSE-100 INDEX: Caution Within Uptrend

Published July 13, 2026

KSE-100 maintains its primary bullish structure following last week's breakout above the 78.6% Fibonacci retracement at 180,993...

KSE-100 INDEX: Rally Eyes Fresh Highs (Technical Weekly)

Published July 6, 2026

KSE100: KSE-100 remains firmly in its primary uptrend after confirming a breakout above the 78.6% Fibonacci retracement at 180,993, reinforcing the prevailing bullish structure...

ENGROH: Breakout Signals Continuation (Flash Note | Pakistan Technicals)

Published July 1, 2026

ENGROH continues to strengthen after recovering from the 302.50-233.00 decline and confirming an upside breakout from a symmetrical triangle...

Economy: Jun-26 Inflation Expected at 11.7% YoY

Published June 30, 2026

The National Consumer Price Index (NCPI) is projected to increase by 11.7% YoY in Jun-26, marking the highest monthly inflation reading of the fiscal year. On a monthly basis, inflation is estimated to rise by 0.2% MoM primarily driven by an uptick in the food segment...

KSE-100 INDEX: Healthy Pullback Continues (Technical Weekly)

Published June 29, 2026

KSE-100 rebounded after finding support at its rising 9-day SMA (178,488), with the latest bullish candle following three sessions of orderly profit taking, indicating buyers remain active on shallow pullbacks...

KSE-100 INDEX: Recovery Trend Holds Firm (Technical Weekly)

Published June 15, 2026

KSE-100 remains in a constructive consolidation phase beneath the 173,100-174,400-resistance zone after repeatedly failing to sustain above the 61.8% Fibonacci retracement level (173,112)...

Federal Budget FY27: From Stability To Growth

Published June 14, 2026

Federal Budget FY27 rotates to growth and offers the biggest relief package since FY21 underwritten by real, booked sources – provincial co-financing and a documented enforcement drive. The consolidated fiscal deficit widens 60bps YoY to 3.6% of GDP and the primary surplus is allowed to shrink 50bps YoY to 2.0%. The 3.6% deficit though contingent on FBR enforcement, seems achievable and is cushioned by overprovisioned debt-service costs and a conservative 8.2% inflation assumption flowing into budget estimates. For equities it is a stock-picker's budget – positive for breadth, not the index: the super tax cut and the largest property stimulus since FY21 favor mid-cap industrials (cement, steel, property, refineries, pharma, IT, value-added textiles), while banks, E&P and fertilizer are excluded from the cut and, at ~55% of KSE-100 weight, cap the index level uplift.

KSE-100 INDEX: Recovery Stalls Near Resistance (Technical Weekly)

Published June 8, 2026

KSE100: KSE-100 has entered a consolidation phase after facing rejection from the 174,400-175,300-resistance zone, with an attempted breakout above the 61.8% Fibonacci retracement level (173,112) of the 191,032-144,119-decline failing to gain traction...

May-26 Domestic Dispatches Plunge 17% YoY to 3.2mn tons due to Eid Holidays

Published June 4, 2026

Pakistan’s domestic cement dispatches stood at 3.2mn tons in May-26, down 17% YoY. The YoY decline is primarily due to high base effect and reduced working days amid Eid holidays...

KSE-100 INDEX: Recovery Trend Strengthens (Technical Weekly)

Published June 1, 2026

KSE100: KSE-100 has extended its recovery trend after decisively surpassing the 61.8% Fibonacci retracement level at 173,112 (derived from the decline between 191,032 and 144,119), breaking above the multi-month descending trendline resistance, and reclaiming and sustaining above its key short- and medium-term moving averages, reinforcing the improving trend structure...

Economy:May-26 Inflation Expected at 11.9% YoY

Published May 25, 2026

The National Consumer Price Index (NCPI) is projected to increase by 11.9% YoY in May-26. On a monthly basis, inflation is estimated to rise by 0.75% MoM, primarily driven by a strong uptick in the food segment. The higher YoY reading is also attributable to the base effect, as inflation in May-25 had eased to 3.5%.

HCAR: 4QMY26 EPS clock in at PKR 7.1, down by 40% YoY, DPS PKR 9/share

Published May 19, 2026

HCAR announced its MY26 result today, where the company reported an EPS of PKR 7.1 in 4QMY26, down 40% YoY. This takes MY26 EPS to PKR 22.6, up 19% YoY. Along with the result the company announced dividend of PKR 9/share.

SLM IPO: Expensive at PKR 19.95/sh; consider indirect exposure via SRVI and SGF

Published May 19, 2026

SLM has strong fundamentals… Service Long March Tyres Limited (SLM) presents a compelling structural investment case anchored in Pakistan’s emerging tariff arbitrage advantage in global tyre trade...

KSE-100 INDEX: Recovery Struggles Higher (Technical Weekly)

Published May 18, 2026

KSE-100 Index remains range-bound after once again failing to sustain above the key 173,000-174,300 resistance zone, aligned with the 61.8% Fibonacci retracement of the last major decline from 191,032 to 144,119...

HCAR: MY26 EPS to rise 19% to PKR23; DPS: PKR 9

Published May 14, 2026

HCAR is expected to announce its MY26 results, where we expect the company to report an EPS of PKR 6.94 in 4QMY26, down 45% YoY. This will take MY26 EPS to PKR 23, up 19% YoY. The company is also expected to announce dividend of PKR 9/share.

CNERGY: Breakout Zone Under Watch (Flash Note | Pakistan Technicals)

Published May 13, 2026

CNERGY has been recovering within a rising channel since forming a major base near 2.60 in 2023 after a prolonged multi-year downtrend from 31.16. Price is currently testing the key 23.6% Fibonacci retracement level near 9.35, aligned with the long-term descending trendline, making this a decisive breakout zone. Sustained strength above 9.50 may open upside toward 10.20–10.30 near the 200-month SMA, which may act as interim resistance, followed by the 38.2% retracement level at 13.50 as the immediate target, where a broader rounding base formation would strengthen. A break above 13.50 may trigger the next bullish leg higher. Strategy favors accumulation on dips toward 8.50-7.90 or buying on a sustained breakout above 9.50, while failure to hold 7.20 may weaken the bullish structure.

KSE-100 INDEX: Recovery Retest Resistance (Technical Weekly)

Published May 11, 2026

KSE-100 Index is once again testing the critical 173,000-174,300 resistance zone, aligned with the 61.8% Fibonacci retracement level (last corrective move from 191,032 to 144,119), where it previously faced rejection in late April before sliding toward the 160,000 region.

KSE-100 INDEX: Corrective Phase, Limited Upside (Technical Weekly)

Published May 4, 2026

KSE-100 is showing a clear loss of follow-through after failing to sustain above 173,500-174,500, slipping back below key moving averages and indicating near-term fatigue...

CHCC: 3QFY26 EPS clocks in at PKR 7.24, down 16% YoY

Published April 29, 2026

CHCC announced its 3QFY26 results, wherein the company reported an EPS of PKR 7.24, down 16% YoY. This takes 9MFY26 EPS to PKR 28.4, down 19% YoY. The company did not announce any dividend for the quarter. However, the Board has recommended a buyback of up to 4% of the paid-up capital (7.77mn shares), subject to shareholder approval at the EOGM scheduled for 9 June 2026.

Economy: SBP increases the policy rate by 100bps

Published April 27, 2026

The State Bank of Pakistan (SBP) announced its monetary policy today, raising the policy rate by 100bps to 11.5%. This marks the first rate hike after nearly two years of monetary easing. The decision reflects SBP’s cautious approach to strengthening the economy’s resilience amid an evolving global landscape while supporting sustainable economic growth.

INDU: 3QFY26 EPS clock in at PKR 85, up by 2% YoY, DPS PKR 51

Published April 27, 2026

INDU announced its 3QFY26 results today, where the company reported an EPS of PKR 85, up by 2% YoY. This takes 9MFY26 EPS to PKR 247 reflecting a 17% YoY increase. Along with the result, the company announced an interim cash dividend of PKR 51/share, taking the cumulative 9MFY26 interim cash dividend to PKR 148/share.

Economy: Apr-26 Inflation Expected at 10.4% YoY

Published April 27, 2026

The National Consumer Price Index (NCPI) is projected to increase by 10.4% YoY in Apr-26. On a monthly basis, inflation is estimated to rise by 2.1% MoM. This is primarily driven by an uptick in the transport segment following the increase in refined oil prices amid heightened geopolitical tensions and the closure of the Strait of Hormuz.

KSE-100 INDEX: Controlled Pullback in Recovery (Technical Weekly)

Published April 27, 2026

KSE-100 has largely followed through on the prior view, sustaining its recovery after reclaiming key moving averages and clearing the 50% retracement taken from the 191,000 high to the 144,100 low, along with the descending trendline.

CHCC: 3QFY26 EPS expected to clock in at PKR 8.26, down 5% YoY

Published April 24, 2026

CHCC is expected to announce its 3QFY26 results, wherein we expect the company to report an EPS of PKR 8.26, down 5% YoY. This will take 9MFY26 EPS to PKR 29.41, down 16% YoY. We do not expect CHCC to announce any dividend for the quarter.

FCCL: 3QFY26 EPS clocks in at PKR 1.41, up 62% YoY

Published April 24, 2026

FCCL announced its 3QFY26 results, wherein the company reported an EPS of PKR 1.41, up by 62% YoY. This takes 9MFY26 EPS to PKR 4.39 up 15% YoY. The company did not announce any dividend for the quarter.

KOHC: 3QFY26 clocks in at PKR 2.03, down 15% YoY

Published April 23, 2026

KOHC announced its 3QFY26 results, wherein the company reported an EPS of PKR 2.03, down 15% YoY. This takes 9MFY26 EPS to PKR 8.06, down 14% YoY. The company did not post any dividend for the quarter.

KOHC: 3QFY26 EPS expected to clock in at PKR 1.98, down 18% YoY

Published April 22, 2026

KOHC is expected to announce its 3QFY26 results, wherein we expect the company to report an EPS of PKR 1.98, down 18% YoY. This will take 9MFY26 EPS to PKR 8.01, down 16% YoY. We do not expect KOHC to post any dividend for the quarter.

INDU: 3QFY26 EPS expected to clock in at PKR 80, down by 5% YoY, DPS PKR 49

Published April 22, 2026

INDU is expected to announce its 3QFY26 results, where we expect the company to report an EPS of PKR 80, down 5% YoY. This will take 9MFY26 EPS to PKR 241, up 15% YoY. The company is also expected to announce an interim cash dividend of PKR 49/share.

MLCF: 3QFY26 Consolidated EPS clocks in at PKR 1.69, down 37% YoY

Published April 22, 2026

MLCF announced its 3QFY26 results, wherein the company reported a consolidated EPS of PKR 1.69*, down 37% YoY. This takes cumulative earnings of 9MFY26 to PKR 7.27/share*, down 3% YoY. The company did not announce any dividend for the quarter, bringing the cumulative dividend per share for 9MFY26 to zero.

MLCF: 3QFY26 EPS expected to clock in at PKR 2.5, down 7% YoY

Published April 21, 2026

MLCF is expected to announce its 3QFY26 results, wherein we expect the company to report a consolidated EPS of PKR 2.5, down 7% YoY. This will take 9MFY26 EPS to PKR 8.06, up 7% YoY. We do not expect MLCF to announce any dividend for the quarter.

PIOC: 3QFY26 EPS clocks in at PKR 6.70, up 56% YoY

Published April 21, 2026

PIOC announced its 3QFY26 results today wherein the company reported an EPS of PKR 6.70, up 56% YoY. This takes cumulative earnings for 9MFY26 to PKR 19.35/share, up 59% YoY. The company did not post any dividend for the quarter, bringing the cumulative dividend per share for 9MFY26 to zero.

SAZEW: 3QFY26 EPS clock in at PKR 106.5, up by 3% YoY, DPS PKR 20

Published April 20, 2026

SAZEW announced its 3QFY26 results today, where the company reported an EPS of PKR 106.5, up by 3% YoY. This takes 9MFY26 EPS to PKR 246, up 16% YoY. Along with the result, the company announced an interim cash dividend of PKR 20/share. This takes 9MFY26 interim cash dividend to PKR 50/share.

KSE-100 INDEX: Recovery Turns Into Rally (Technical Weekly)

Published April 20, 2026

KSE-100 has delivered the expected follow-through, decisively reclaiming the 100-day SMA and breaking above the 50% retracement along with the descending trendline, signaling strengthening recovery and a shift back toward trend continuation after the corrective phase

PIOC: Volumetric Growth to Lead 52% YoY Increase in Earnings

Published April 17, 2026

PIOC is expected to announce its 3QFY26 results, wherein we expect the company to report an EPS of PKR 6.53, up 52% YoY. This will take 9MFY26 EPS to PKR 19.18, up 57% YoY. We do not expect PIOC to post any dividend for the quarter.

FCCL: Surge in Dispatches and Other Income to Boost Earnings 64% YoY

Published April 16, 2026

FCCL is expected to announce its 3QFY26 results, wherein we expect the company to report an EPS of PKR 1.43, up by 64% YoY. We do not expect FCCL to declare any dividend along with the result.

Cement Universe to Post Earnings of PKR 10.3bn in 3QFY26, up 3% YoY

Published April 14, 2026

Akseer’s Cement Universe is expected to post earnings of PKR 10.3bn in 3QFY26, up 3% YoY. Net sales will likely rise, 8% YoY in 3QFY26, supported by 7% YoY growth in local dispatches and 4% YoY increase in cement prices. The growth in net sales was limited due to halt in exports to Afghanistan following border closure.

SAZEW: 3QFY26 EPS expected to clock in at PKR 113, up by 11% YoY, DPS PKR 23

Published April 13, 2026

SAZEW is expected to announce its 3QFY26 results, where we expect the company to report an EPS of PKR 113, up 11% YoY. This will take 9MFY26 EPS to PKR 254, up 19% YoY. The company is also expected to announce an interim cash dividend of PKR 23.00/share.

KSE-100 INDEX: Strong Recovery Seen, Key Test Ahead (Technical Weekly)

Published April 13, 2026

KSE-100 is testing a confluence of critical resistance at the 100-day SMA (~169,650), aligned with the 50% Fibonacci retracement (191,023–144,119 corrective move), after staging a strong ~11% weekly rebound, while reclaiming the 200- and 50-day SMAs; improving volumes and RSI near the 60s signal strengthening momentum. Immediate resistance stands at 168,300-169,700, and a sustained break above this zone is required to extend recovery toward 171,500–173,100, where the descending trendline and 61.8% retracement converge. On the downside, the 50-day SMA (~164,800) offers initial support, followed by the critical 162,000-160,600 demand zone; a break below this range would turn the outlook cautious. Bias remains positive above this zone, though partial profit-taking is advised near higher resistance.

KSE-100 INDEX: Consolidation with Bearish Tilt (Technical Weekly)

Published April 6, 2026

The KSE-100 Index maintains a corrective bias after sustaining below the rising channel support, reaffirming a short-term bearish shift within a broader uptrend. Price continues to hover around the 50-week SMA (~152k) with no meaningful recovery, while RSI remains subdued, indicating weak momentum. The 50% retracement at 146,315 remains pivotal; holding above it keeps the structure intact, otherwise downside may extend towards 135,700-132,600. On the upside, 156k-158k remains immediate resistance, followed by a stronger supply zone at 161k-163k near the gap area. The prior strategy remains valid: sell on strength below 158k, with a cautious stance unless a decisive reclaim above 158k improves sentiment.

KSE-100 INDEX: Intraweek Update (Flash Note | Pakistan Technicals)

Published April 1, 2026

Not to be tempted by short-term positive spells, a clear perspective should be taken on current price action. Index levels are trading below the 200-dema (156,461) which in itself is a red flag. Further, a polarity shift has taken place around 157,800 from support to resistance. Moving onto the third step of caution, current price moves are moving within a triangle formation and unless an upward break above 157,800 is witnessed, the developing course of direction remains weak and prone to a downward break. Closings below 145k pave way for the formation to trigger on the downside. Keep a cautious stance looking for clarity on the upside before entering long.

Economy: Mar-26 Inflation Expected at 7.2% YoY

Published March 30, 2026

The National Consumer Price Index (NCPI) is projected to increase by 7.2% YoY in Mar-26. On a monthly basis, inflation is estimated to rise by 1.08% MoM, primarily driven by sharp pressures in the transport segment amid escalating geopolitical tensions in the Middle East.

KSE-100 INDEX: Sustain Break Validates Earlier Reversal Signals (Technical Weekly)

Published March 30, 2026

The KSE-100 Index has turned bearish following a confirmed break below channel support, signaling a shift from the prior strong uptrend. The index is now testing the 50-week SMA around 152k, which is being closely tracked, while the key level remains the 50% retracement at 146,315 of the prior uptrend from 101,598 to 191,032, holding above keeps the broader structure intact. Momentum remains weak, suggesting limited upside. On the higher side, 156k to 158k is immediate supply, with 161k to 163k gap acting as a strong cap. Strategy stays sell on strength below 158k. A weekly close below 146,315 exposes downside towards 135,762 to 132,626, while holding above may keep the index range bound between 146k to 158k.

KSE-100 INDEX: The Cyclical Shift (Technical Weekly)

Published March 16, 2026

Since gaining above the 40-wema in July 2023 the last two weeks have witnessed the first cyclical shift below the key average. This shift took place after a downside gap from 161,476 – 162,953 that stands above the key average. This window stands as a key resistance to close above if the index has to reestablish support above the key average. Immediate resistance though is at the 40-wema (158,055). Looking on the downside, we measure two key uptrends – one from the major low at 35,153 (Jan. ‘23) and the second from 101,599 (May ‘25) to the peak at 191,032. The latter trend has corrected 50% at 146,315 and holds which defines the current support area. Thus, weekly close below 146,315 deepens the correction towards 135,762 (61.8%). This latter level coincides with the broader trend from 35,153 that corrects 38.2% at 132,626. Over the short-term we can expect a range from 146,315-158,00 while an expanding cyclical shift on the downside would look towards 132,626-135,762.

Economy SBP maintains Status quo at 10.5%

Published March 10, 2026

The State Bank of Pakistan (SBP) announced its monetary policy today, deciding to maintain the benchmark policy rate at 10.5%, in line with market expectations. This decision underscores the SBP’s cautious and prudent approach, aimed at increasing the economy’s resilience to shocks.

KSE-100 INDEX: Downside Risk Remains Elevated (Technical Weekly)

Published March 2, 2026

KSE-100 extended its corrective trajectory and decisively breached the 170,000 to 169,500 demand cluster, effectively negating the prior rebound thesis and confirming short term trend deterioration following rejection near the wedge top. The index briefly traded below the rising 30 week SMA (165,690), printing an intraday low near 162,950 before settling at 168,062, highlighting elevated volatility and visible distribution. Momentum continues to soften as RSI drifts toward neutral, reflecting fading upside conviction. Near term resistance is now aligned between 170,000 and 173,000, with 179,000 as the next upside cap, while support is concentrated between 165,700 and 163,900. A sustained break below this band may accelerate decline toward 156,300 and potentially the 50-week SMA (149,068). Bias turns cautious; prefer selling into strength below 173,000, while accumulation is warranted only on a decisive recovery above 173,000 with improving momentum.

Economy: Feb-26 Inflation Expected at 6.5% YoY

Published February 27, 2026

The National Consumer Price Index (NCPI) is projected to increase by 6.5% YoY in Feb-26. On a monthly basis, inflation is estimated to decline by 0.23% MoM, primarily driven by decline in food prices. Given the prevailing policy rate of 10.5%, the real interest rate is estimated at approximately 4.0%.

KOHC: 2QFY26 EPS clocks in at PKR 2.82, down by 21% YoY

Published February 25, 2026

KOHC announced its 2QFY26 results today wherein the company reported an EPS of PKR 2.82, down by 21% YoY.

FCCL: 2QFY26 EPS clocks in at PKR 1.64, flattish YoY

Published February 25, 2026

FCCL announced its 2QFY26 results today wherein the company reported an EPS of PKR 1.64, flattish YoY.

Net sales for 2QFY26 clocked in at PKR 23.9bn, down 4% YoY from PKR 24.9bn in SPLY. The YoY decline in net retention due to depressed regional prices is partially offset by a 9% YoY growth in local dispatches, clocking in at 1.5mn tons in 2QFY26.

Gross margins for 2QFY26 clocked in at 35%, down from 36% in SPLY due to lower retention and upward pressure on coal prices caused by Afghan border closure.

Finance costs clocked in at PKR1.1bn, down by 19% YoY owing to a decline in interest rates and deleveraging of the balance sheet.

On a sequential basis, earnings are up 22% QoQ. Net revenue marginally increased by 2% QoQ where 18% QoQ growth in local dispatches was offset by 83% QoQ decline in exports due to Afghan border closure.

We maintain a ‘Buy’ recommendation on the stock based on our Dec-26 price target (PT) of PKR 67/share.

MLCF: 2QFY26 EPS clocks in at PKR 2.98, down by 16% YoY

Published February 25, 2026

MLCF announced its 2QFY26 results today wherein the company reported an EPS of PKR 2.98, down by 16% YoY.

KSE-100 INDEX: Demand Cluster in Focus (Technical Weekly)

Published February 23, 2026

KSE-100 extended its corrective phase for a fourth consecutive week following the bearish engulfing formation near the wedge top (week ended Jan 26), with price testing the anticipated demand zone around 170,000 and recording an intraday low near 169,600. This area reflects strong confluence, aligning with the 100-day SMA, the 61.8% retracement of the 157,200-191,000 advance, and horizontal support from the December breakout. Holding above 170,000 may trigger a relief rebound toward 179,000-181,243, where the 9-week SMA caps near-term upside, while a stronger recovery could expose a wedge support retest near 187,000. Immediate supports stand at 170,000 and 169,500, followed by 165,690 near the rising 30-week SMA; a sustained break below this average may extend deeper correction toward 156,000. Strategy remains cautious, favoring selective accumulation above 169,500 with strict stops and booking profit near resistance.

KSE-100 INDEX: Retracement Phase Tests Structural Support (Technical Weekly)

Published February 16, 2026

KSE-100 has extended its corrective phase from the wedge top, reinforcing near-term distribution within the broader uptrend. The decisive break below the 9-week SMA tilts short-term control to sellers, with price now testing the 38.2% retracement near 178,000, derived from the 157,200-191,000 impulsive leg. Sustained trade below this zone would expose deeper retracement risk. Weekly RSI continues to ease from overbought levels, maintaining bearish divergence. Immediate resistance is placed at the 9-week SMA (181,047) and 183,500, levels that are likely to be tested in the coming sessions if rebound attempts persist, while major supply remains at 188,000-191,000. Key support stands at 178,000, followed by 174,000-170,000 on breakdown. Strategy favors selling into strength below 188,000 and avoiding aggressive longs until stabilization emerges.

PIOC: 2QFY26 EPS clocks in at PKR 7.04, down 9% YoY

Published February 11, 2026

PIOC announced its 2QFY26 results today wherein the company reported an EPS of PKR 7.04, down 9% YoY. This takes cumulative earnings for 1HFY26 to PKR 12.65/share, up 4% YoY. Contrary to expectations, no dividend was announced along with the results.

KSE-100 INDEX: Follow-Through Reinforces Cautious Stance (Technical Weekly)

Published February 9, 2026

The KSE-100 has shown a follow-through after last week’s bearish engulfing near the upper boundary of the rising wedge, reinforcing signs of short-term exhaustion within the broader uptrend. Price remains inside the wedge and above the 9-week SMA, so the primary structure is still intact, but momentum continues to weaken with the weekly RSI holding bearish divergence near overbought territory. This keeps the near-term bias cautious as long as the index trades near the wedge top. Immediate resistance is seen at 188,000-191,000, while key support lies at 181,000-179,500 around the wedge base and 9-week average. A decisive break below this zone may trigger a deeper correction toward 174,000-171,000, while only a sustained move above 191,000 would negate the wedge risk. Strategy favors reducing exposure into strength and waiting for dips toward support for selective re-entry.

20260202095548.png)

KSE-100 INDEX: Corrective Risk Builds After Extended Run (Technical Weekly)

Published February 2, 2026

The KSE-100 index has printed a bearish engulfing candle near the upper boundary of a rising wedge, signaling potential trend exhaustion. This is reinforced by a clear bearish divergence on the weekly RSI, supporting a near-term corrective or reversal risk. The 9-week SMA around 178,071, aligning with wedge support, remains a critical pivot; a decisive break below would confirm a bearish reversal and open the door for a deeper correction. Immediate resistance is seen at 187,200–188,000, while a sustained close above 191,100 would invalidate the bearish setup. Initial support lies at 181,000–180,500. Strategy favors capital preservation, avoiding fresh longs near highs, reducing exposure into strength, and considering selective re-entry only if price stabilizes above wedge support and key moving averages.

Economy: Jan-26 Inflation Expected at 6.0% YoY

Published January 30, 2026

The National Consumer Price Index (NCPI) is projected to increase by 6.0% YoY in Jan-26. The monthly inflation is estimated at 0.54% MoM, primarily driven by higher food prices. Given the prevailing policy rate of 10.5%, the real interest rate is estimated at approximately 4.5%.

Cement Universe to Post Earnings of PKR 12.4bn in 2QFY26, down 18% YoY

Published January 30, 2026

Our Cement Universe is expected to post earnings of PKR 12.4bn in 2QFY26, down 18% YoY primarily due to weaker retention amid lower cement prices, disruptions in export volume and higher coal prices due to Afghan border closure, and decline in other income caused by lower interest rates.

Economy: SBP maintains Status quo at 10.5%

Published January 27, 2026

The State Bank of Pakistan (SBP) announced its monetary policy today, deciding to maintain the benchmark policy rate at 10.5%, contrary to market expectations. This decision underscores the SBP’s cautious and prudent approach, aimed at safeguarding price stability while supporting sustainable economic growth.

20260126194608.jpg)

SAZEW: 2QFY26 EPS expected to clock in at PKR 94, up by 136% YoY, DPS PKR 26

Published January 27, 2026

SAZEW is expected to announce its 2QFY26 results, where we expect the company to report an EPS of PKR 93.8, up by 136% YoY. Along with the result, the company is expected to announce an interim cash dividend of PKR 26.00/share.

20260126115103.png)

KSE-100 INDEX: Trend Strengthens After Supply Absorption (Technical Weekly)

Published January 26, 2026

The KSE-100 index continues to trade with a strong bullish tone, as price has pushed higher and registered fresh all-time high closes on both daily and weekly timeframes, confirming continuation of the broader uptrend. The index has now absorbed the earlier supply area around 186,200-187,900, keeping the path open for a gradual move toward 192,000-195,000 and potentially 198,000. Importantly, the weekly RSI has broken above its resistance trendline connecting previous lower highs, indicating renewed momentum strength and invalidating the earlier bearish divergence. Any dips toward 186,000-184,500 are likely to attract buying interest, while the 180,900-180,590 zone remains a critical medium-term support. The preferred approach remains to accumulate on pullbacks within the uptrend and trail stops higher, as only a sustained break below 178,400 would indicate a shift toward a deeper corrective phase.

KSE-100 INDEX: Pullback Absorbed, Uptrend Structure Holds (Technical Weekly)

Published January 19, 2026

The KSE-100 index retains a constructive bullish structure after a shallow pullback that found support in the 180,900-180,590 zone, followed by a rebound to close at a fresh weekly high near 185,098. This recovery, despite the ongoing bearish divergence on the weekly RSI highlighted earlier, indicates consolidation within the prevailing trend rather than a reversal. Near-term supply is expected around 186,200-187,900, while a sustained move above 188,000 is required to reassert upside momentum toward the 192,000-197,000 zone. On the downside, immediate support is placed at 183,600, with 180,900-180,590 as the key demand area; a sustained break below 178,400 would signal a deeper corrective phase.

KSE-100 INDEX: Uptrend Slows as Resistance Caps Momentum (Technical Weekly)

Published January 12, 2026

The KSE-100 index remains in a primary uptrend, trading above its rising 9- and 30-week moving averages within a well-defined upward channel. However, the latest weekly candle shows rejection near the 227.2% Fibonacci extension around 187,365, aligned with resistance drawn from recent swing highs, signaling short-term exhaustion. This is reinforced by a bearish divergence on the weekly RSI, highlighting slowing momentum at elevated levels. In the near term, a cautious buy-on-dip approach is preferred, with 182,600-180,900 as immediate support. The 178,400 level remains critical, as a sustained break below this level would likely lead to a deeper corrective phase. On the upside, 185,300–186,100 is immediate resistance, while a sustained close above 188,000 would revive upside potential toward 192,000 and 197,000.

KSE-100 INDEX: Strength Continues Within Rising Channel (Technical Weekly)

Published January 5, 2026

The KSE-100 Index extended its primary weekly uptrend, closing at a fresh all-time high near 179,000 while holding firmly above the 400% Fibonacci extension at 170,143, keeping last week’s constructive bias intact. The move is supported by the rising 9-week SMA, a well-defined ascending channel, and firm weekly volumes, reflecting sustained institutional participation despite a stretched condition. The broader structure continues to favor buy-on-dip strategies as long as the index holds above the 167,000-170,000 support band. On the upside, immediate resistance is seen near the 461.8% Fibonacci extension around 180,700, with sustained acceptance above 181,000 opening room toward the upper channel zone at 187,000-190,000. A decisive weekly close below 165,000 would signal emerging trend fatigue and warrant caution.

Economy: Dec-25 NCPI Expected at 5.8% YoY

Published December 31, 2025

The National Consumer Price Index (NCPI) is expected to ease to 5.8% YoY in Dec-25. On a monthly basis, inflation is projected at -0.29% MoM. The sequential decline is to be driven mainly by lower food prices. Based on the projected Dec-25 inflation level and the surprise rate cut of 50bps by SBP, the real interest rate is estimated at 4.7%.

Strategy: Transitioning from Survival to Growth

Published December 31, 2025

Pakistan’s equity market is transitioning from a liquidity driven rally to earnings led phase. After a strong 52% return by the KSE 100 in CY25, supported by sharp rate cuts, valuation normalization, and improving macro stability, momentum remains positive but expectations are now more measured. We set a CY26 KSE 100 target of 211,042 points, implying around 22% return. With limited appeal in fixed income and real estate, liquidity should continue to favor equities. However, returns are likely to be selective, rewarding companies with strong balance sheets, pricing power, and cash flow visibility, as reforms progress gradually and execution remains the key determinant for sustainable growth.

KSE-100 INDEX: Bullish Structure with Measured Follow-Through (Technical Weekly)

Published December 29, 2025

The KSE-100 Index traded within a narrow range and remained below last week’s candle peak, while posting fresh daily and weekly closing highs near 172,400. Price continues to hold comfortably above the 400% Fibonacci extension at 170,143, which now acts as immediate support, followed by the rising 9-week SMA near 165,855 as the critical medium-term support, confirming sustained buying interest. Momentum remains strong but extended, favoring continuation with selective risk management. The broader uptrend remains intact as long as the index holds above the 166,000-170,000-support band. On the upside, the next objective lies at the 180,700 Fibonacci extension, followed by the upper channel region around 187,000-190,000. A decisive weekly close below 165,000 would signal trend weakening.

KSE-100 INDEX: Momentum Holds Within Rising Channel (Technical Weekly)

Published December 22, 2025

The KSE-100 Index extended last week’s advance, marking a fresh all-time high at 172,674.65 before consolidating modestly, while the dominant uptrend within the rising channel remains firmly intact. Price continues to hold above the 9-week SMA, reflecting trend persistence rather than exhaustion, with weekly volumes remaining supportive of the broader move. The 168,000-169,000 zone now stands as the primary near-term support, representing the recent breakout area, while 163,000-164,000 remains the key structural floor sustaining trend integrity. On the upside, consolidation below the 170,000-172,700 supply band suggests healthy digestion; a decisive weekly close above this zone would reinforce continuation toward the 180,700 Fibonacci projection and eventually the upper channel boundary near 187,000–189,000. A weekly close below 163,000 would weaken the setup.

EPCL: Reversal Structure Unfolds (Flash Note | Pakistan Technicals)

Published December 19, 2025

EPCL (LDCP 35.77) price has confirmed a bullish reversal by breaking above the long-term falling wedge resistance near 34.50-35.00. The wedge’s measured move projects an upside target toward 51.47-53.00, the former level being the 38.2% retracement for the overall bear trend. The 35.00 zone now acts as key support, where pullbacks may offer accumulation opportunities. A close below 31.00 would negate the breakout and defines downside risk.

PIBTL: Gushing The Saucer (Flash Note | Pakistan Technicals)

Published December 18, 2025

The stock is undergoing a cyclical shift in direction from a long-term bear trend that persisted between 2015 till 2023. The focus, though, is on the phase from Sep. ’20 till Sep. ’25 during which price formed a saucer formation. The neckline for this pattern is at 14.30 which received clear breakouts in October and retests of this breakout in November.

Economy: SBP slashes policy rate by 50bps

Published December 16, 2025

The State Bank of Pakistan (SBP) announced its monetary policy today (Monday), cutting the benchmark policy rate by 50bps to 10.5%. This move marks an unexpected rate adjustment after the policy rate had remained unchanged at 11% since May-25.

Some key developments influencing the MPC’s decision include: (i) average inflation remaining within the target range during Jul–Nov of FY26, and (ii) continued benign global commodity prices.

KSE-100 INDEX: Renewed Strength Signals Continuation Potential (Technical Weekly)

Published December 15, 2025

The KSE-100 Index resumed its recovery after last week’s brief pause, posting a fresh all-time high at 170,697 and closing at a new weekly high of 169,864, reinforcing the dominant uptrend within the rising channel. Improving weekly volume underscores strengthening participation and supports the constructive momentum as price holds firmly above the 9-week SMA, keeping 163,000–164,000 as the primary demand zone. The index is now pressing into the 168,400–170,000 supply shelf, where a decisive close above 170,500 is still required to unlock upside toward the 180,700 Fibonacci marker and the rising channel top, which is projected around 187,000–189,000 for next week. Until such a breakout, controlled dips toward support remain buyable, while a close below 163,000 would soften near-term momentum.

KSE-100 INDEX: Momentum Builds as Market Awaits Confirmation (Technical Weekly)

Published December 8, 2025

The KSE-100 Index maintained its constructive tone as price held above the 9-week SMA, keeping last week’s improving momentum intact and reaffirming the 163,000-164,000 band as the key near-term support zone. The broader uptrend within the rising channel remains dominant, with the index gradually consolidating below the 168,400-170,000 supply region. This area continues to cap upside attempts, and only a decisive weekly close above 170,500 would confirm trend acceleration toward the 180,700 Fibonacci extension, followed by the channel resistance near 185,000–187,000. Until such a breakout occurs, the index may continue to drift within a tight range, where controlled pullbacks into 163,000-164,000 can offer selective accumulation. Bias stays positive above this support cluster, while a breach below it would temporarily weaken momentum and delay further upside progress.

KSE-100 INDEX: Bullish Tone Reemerges After Key Reclaim (Technical Weekly)

Published December 1, 2025

The KSE-100 Index staged a strong rebound this week, reclaiming the 9-week SMA near 163,460 and establishing the 163,000 to 164,000 zone as immediate support for the near term. This recovery improves short-term momentum and keeps the index positioned to retest the 168,400 to 170,000 region, which represents a critical supply zone formed by the October 20 high and the September 29 peak. A sustained break above 170,500 would confirm renewed bullish momentum and open the way toward the 461.8% Fibonacci extension near 180,734, followed by the channel top in the 185,000-187,000 area. Price action remains constructive above the newly reclaimed support, and any pullback toward 163,000 to 164,000 may offer selective accumulation opportunities, while a cautious stance is still appropriate until a clear breakout above 170,500 is achieved.

Economy: Nov-25 NCPI Expected at 6.4% YoY

Published November 28, 2025

The National Consumer Price Index (NCPI) is expected to clock in at 6.4% YoY in Nov-25. On a monthly basis, inflation is projected at 0.65% MoM. The MoM increase is primarily driven by higher food prices, reflecting both the lingering impact of earlier floods and the disruptions caused by the Afghan border closure.The State Bank of Pakistan (SBP) expects inflation to remain within the 5–7% range for FY26, although it is likely to exceed the upper band of the target range for a few months during the fiscal year.

Economy: Inflation Risk Real or Just a Fear?

Published November 28, 2025

Pakistan is at a pivotal moment in determining the direction of its exchange rate. While the rupee has long been associated with inflationary spikes whenever devalued, the present macroeconomic context signals a limited inflationary transmission from PKR depreciation. Since domestic food prices have already adjusted by 26.5% beyond global benchmark, the scope for additional inflationary pressure from depreciation remains limited. In this environment, a carefully managed depreciation of the rupee could support export competitiveness, attract higher remittance inflows, and strengthen the external account, offering a strategic opportunity to devalue the currency without immediately destabilizing prices.

KSE-100 INDEX: Sideways Phase Continues with Cautious Tone (Technical Weekly)

Published November 24, 2025

The KSE-100 Index remains in a consolidation phase and continues to hold above the 23.6% Fibonacci retracement near 157,200, preserving the broader bullish structure. Last week’s marginal gain closing at 162,102 shows stability, although the index is still trading below the 9-week SMA at 162,968, keeping immediate pressure intact. The latest weekly candle reflects indecision, and resistance between 162,900 and 164,000 must be cleared to re-establish upward momentum and allow a retest of the 169,988 to 170,000 region before any continuation toward the upper channel band. As long as 157,000 remains intact, the bias stays neutral to constructive, while a breakdown below this level could deepen the correction toward the 50% retracement near 142,400 and the 30-week SMA. Softening volumes and a moderating RSI support a cautious approach, with staggered accumulation only near support and risk managed below 157,000.

KSE-100 INDEX: Bulls Defend Base, Momentum Still Soft (Technical Weekly)

Published November 17, 2025

The KSE-100 Index continues to consolidate and is holding above the 23.6% Fibonacci retracement at 157,200, the first line of defense. Last week’s mild recovery saw the index gain 1.47% to close at 161,935, but it remains below the 9-week SMA at 162,516. Immediate resistance is located between 162,500 and 163,900, and a sustained breakout above this area is needed to regain upward momentum and retest the 169,988 to 170,000 zone, a critical psychological barrier. A confirmed close above that level paves the way for a move toward the channel top near 180,000 to 182,000. On the downside, a break below 157,000 could trigger a deeper corrective phase toward the 50% retracement and the 30-week SMA around 143,000 to 141,000. Weakening volumes and a cooling RSI support the consolidation narrative. A measured approach is advised, with staggered accumulation near support and risk kept below 157,000, while short-term upside should be viewed cautiously until strength visibly returns.

KSE-100 INDEX: Pullback Deepens Amid Waning Momentum (Technical Weekly)

Published November 10, 2025

The KSE-100 Index slipped below the 9-week SMA for the first time since early May 2025, signaling short-term momentum loss after a strong advance earlier this year. The index’s 23.6% Fibonacci retracement zone, measured from the June 23 low near 115,900 to the October 25 peak around 169,990, lies between 157,200 and 156,300, aligning with last week’s low and offering initial support. A decisive break below this area could extend the correction toward the 50% retracement near 142,900 and the 30-week SMA around 139,500. Immediate resistance is seen near the 9-week SMA at 161,600–162,000, followed by 165,500, where a sustained close above would reaffirm upside momentum toward 168,600–170,000. Trading volume has declined for three consecutive weeks, reflecting subdued participation amid consolidation. A cautious near-term stance is advised; measured accumulation may be considered near 157,200, with risk defined below 156,000.

KSE-100 INDEX: Gap-Up Rally Signals Momentum Revival (Technical Weekly)

Published November 3, 2025

The KSE-100 Index rebounded sharply after finding support near 156,732, aligning with the lower boundary of the short-term descending channel. The index opened the last session with a pro gap and formed a bullish sash candlestick pattern, signaling a potential reversal from short-term weakness. Despite closing slightly below the 9-day SMA at 162,321, momentum has improved as RSI broke above its descending trendline, indicating a short-term positive shift. Immediate resistance is seen at the 30-day SMA around 163,318, followed by the upper boundary of the descending channel near 167,500, while the 168,600-170,000 zone remains a major supply area that must be cleared for the next leg higher. On the downside, 159,200 and 156,700 serve as key supports. Overall, the broader trend stays bullish within the rising channel, and short-term dips toward support may offer buying opportunities, with a sustained break above 169,000 needed to reignite momentum toward new highs.

Economy: Oct-25 NCPI Expected at 5% YoY

Published October 30, 2025

The National Consumer Price Index (NCPI) is expected to remain slightly elevated at 5% YoY in Oct-25. On a monthly basis, the inflation is projected to clock in at 0.6% MoM. The State Bank of Pakistan (SBP) estimates an inflation outlook in the range of 5-7% for FY26, though inflation is expected to fall above the upper limit of the target range for a few months of this fiscal year. Based on this inflation outlook of 5% for Oct-25, the real interest rate is projected to be 6%. Meanwhile, core inflation is expected to persist at 8.0% YoY in Oct-25, reflecting the underlying price stickiness.

Economy: SBP maintains policy rate at 11%

Published October 27, 2025

The State Bank of Pakistan (SBP) announced its monetary policy today, wherein the benchmark policy rate was kept unchanged at 11% for the fourth consecutive time.

KSE-100 INDEX: Steady Uptrend Consolidates before Next Move (Technical Weekly)

Published October 27, 2025

The KSE-100 continued to consolidate after testing the channel top around 169,989, which coincides with the 400% Fibonacci extension level from the week ended September 29. The index is holding firmly above the 9-week SMA at 159,647 and the 300% Fibonacci extension near 153,000, both acting as key support levels. The overall trend remains bullish within the rising channel, though a clear breakout above 170,500 is required to confirm the next upward leg. RSI has cooled off from 88.20 to 76.48, reflecting moderation in momentum after a strong rally, while volumes suggest healthy participation during the pause. Bulls may stay positioned on the long side, adding on retracements toward 159-153k with stops below 153k, and consider partial profit-taking around 166–170k; a weekly close below 153k could trigger a deeper corrective phase.

SAZEW: PHEV Expansion and Cost Discipline Driving Growth Uphill

Published October 24, 2025

Groundwork to Grid Power: Entering the Plug-In Era

We initiate coverage on Sazgar Engineering Works Limited (SAZEW) with a ‘BUY’ recommendation and a target price of PKR 2,690/share for June ‘26, representing potential upside of 40%. Our positive outlook is underpinned by i) SAZEW’s expansion in the PHEV market through the introduction of TANK-500 and Cannon Alpha in Completely Knocked Down (CKD) form, ii) strengthening HAVAL’s market position translating into higher sales, and iii) SAZEW navigating margin decline through production efficiency and localization.

KSE-100 INDEX: Trend Resilient as Bulls Hold Key Support (Technical Weekly)

Published October 20, 2025

The KSE-100 Index posted a mild rebound this week, closing at 163,806, up 0.43%, after testing support near the 9-week SMA at 158,100. The price action suggests consolidation within the upper band of the ascending channel, following rejection at the 400% Fibonacci extension (170,100). The RSI has cooled slightly from overbought levels but remains elevated at 77, indicating continued strength, though with signs of waning momentum. The broader trend stays firmly bullish as long as the index maintains its position above the 30-week SMA (135,000).

KSE-100 INDEX: Resistance Halts Advance, Supports in Focus (Technical Weekly)

Published October 13, 2025

The KSE-100 index lost momentum this week, slipping 3.49% to close at 163,098 after failing to sustain above the 400% Fibonacci extension near 170,100. This pullback reflects profit-taking near the upper boundary of the rising channel, where the RSI had entered overbought territory. Despite the decline, the broader structure remains bullish as long as the index holds above the 9-week moving average at 156,200, which continues to act as strong support within the ongoing uptrend.

KSE-100 INDEX: Rising Channel Points to Extended Upside (Technical Weekly)

Published October 6, 2025

The KSE-100 ended the week at 168,990 after touching 169,988, extending its climb within the rising channel. The index has cleared the 361.8% Fibonacci extension at 163,900 and is now testing the 400% level at 170,100. A sustained move above this zone can pave the way toward the 461.8% extension at 180,700. The upper boundary of the channel, slightly adjusted, aligns with this level, indicating further upside room remains intact. Still, with RSI hovering at 88, the market is in overbought territory, raising the risk of short-term volatility or consolidation despite the underlying bullish trend.

KSE-100 INDEX: Rally Extends Toward Channel Top (Technical Weekly)

Published September 29, 2025

The KSE-100 closed the week at 162,257 after marking a new high of 162,422, extending its rally within the rising channel. Price action has moved firmly past the 161,000-163,600 zone outlined earlier, supported by rising volumes, though RSI at 86 highlights overheated conditions. The broader trend remains bullish, yet the market’s stretched momentum increases the probability of near-term consolidation or mild retracement without altering the underlying strength.

PIOC: 4QFY25 EPS clocks in at PKR 4.98 down by 16% YoY, DPS PKR 10.0

Published September 26, 2025

PIOC announced its 4QFY25 financial result today wherein the company reported an EPS of PKR 4.98, down by 16% YoY. This takes cumulative earnings of FY25 to PKR 21.47/share, down by 6% YoY. Along with the result, the company announced a cash dividend of PKR 5/share, taking cumulative payout for FY25 to PKR 10/share.

KSE-100 INDEX: Uptrend Strong with Room to Extend (Technical Weekly)

Published September 22, 2025

The KSE-100 continued its upward momentum, closing the week at 158,037 after making a new high of 159,337. The index remains firmly positioned within the rising channel, with price action now approaching the 161,000-163,600 zone, marked by Fibonacci extension and the upper boundary of the channel. RSI has further extended into overbought territory at 84, suggesting the market is running hot, where short-term pullbacks or sideways consolidation cannot be ruled out despite the intact bullish structure.

Economy - SBP maintains policy rate at 11%.

Published September 16, 2025

The State Bank of Pakistan (SBP) announced its monetary policy on Monday, wherein the benchmark policy rate was kept unchanged at 11% for the third consecutive time.

KSE-100 INDEX: Shooting Star Hints at Near-Term Caution (Technical Weekly)

Published September 15, 2025

The KSE-100 index posted a fresh all-time high at 157,816 before settling at 154,440, holding firm above the 153,000 breakout zone. The broader trend remains bullish within the rising channel, with price supported by the 9- and 30-week moving averages. However, the latest weekly candle has formed a shooting star pattern, reflecting signs of exhaustion at elevated levels. Coupled with an RSI reading near 83, the setup points to stretched momentum where short-term volatility or profit-taking cannot be ruled out, even as the broader structure favors buyers.

KSE-100 INDEX: Rising Channel Fuels Continued Rally (Technical Weekly)

Published September 8, 2025

The KSE-100 index rebounded strongly in the latest week, adding 5,659 points and closing at 154,277, marking a fresh all-time high after clearing the 151,200-resistance zone and testing above the 300% Fibonacci extension at 153,007. The uptrend remains firmly intact within the rising channel, with price action supported by both the 30- and 50-week moving averages. RSI has surged further to 82.74, reflecting stretched momentum conditions and raising the probability of interim profit-taking; however, the persistence of strong upward momentum continues to signal sustained buying interest.

KSE-100 INDEX: Market Consolidates After Multi-Week Rally (Technical Weekly)

Published September 1, 2025

After nine consecutive positive weeks, the KSE-100 index posted a pause, retracing from the previous high of 151,261 and finding strong support at 147,209, where buyers stepped in to defend the uptrend, leading to a weekly close at 148,617 with a decline of 875.28 points. The rebound from this dip reinforces bullish sentiment as the index holds above the 261.8% Fibonacci extension at 146,461 while consolidating within the rising channel. The RSI remains elevated at 79.92, indicating persistent overbought conditions and increasing the likelihood of profit-taking on strength, although overall momentum remains intact.

Economy: Aug-25 NCPI expected at 3.7% YoY

Published August 27, 2025

The National Consumer Price Index (NCPI) is expected to clock in at 3.7% YoY in Aug-25. On a monthly basis, the inflation in the month is projected to remain at 0.01% MoM. The State Bank of Pakistan (SBP) estimates an inflation outlook in the range of 5-7% for FY26. Based on the inflation outlook at 3.7% for Aug-25, the real interest rate is projected to be 7.3%.

KSE-100 INDEX: Market Extends Gains, Eyes Next Resistance Zone (Technical Weekly)

Published August 25, 2025

The KSE-100 index extended gains for another week, closing at 149,493 after marking a high of 151,261, maintaining strength above the 261.8% Fibonacci extension at 146,461. The index remains positioned in the upper band of the rising channel, confirming the prevailing bullish trend despite an RSI reading of 81.84, which continues to indicate overbought conditions and a heightened risk of near-term pullbacks. Volume remains healthy, supporting the ongoing trend, though momentum may face resistance as the index approaches the 300% Fibonacci projection at 153,007.

KSE-100 INDEX: Uptrend Intact with Caution of Pullback (Technical Weekly)

Published August 18, 2025

The KSE-100 index extended its advance, gaining 1,109 points to settle at 146,491 after registering a high of 147,977, consolidating above the 261.8% Fibonacci extension at 146,461. Price action remains well-positioned within the upper band of the rising channel, keeping the bullish trajectory firmly intact. The weekly RSI has risen further to 80.33, underscoring strong momentum but also signaling overbought conditions that raise the probability of short-term pullbacks. Volume patterns suggest steady participation, though signs of exhaustion could emerge near immediate resistance.

Pakistan's Motorcycle Revival: Demographics Meet Economic Recovery

Published August 15, 2025

Stellar Motorcycle Volume Growth Likely between FY26-29: Helped by demographic tailwinds, high sensitivity to economic recovery and the need for urban mobility, we project 63% cumulative motorcycle sales growth by FY29, translating to FY26-29 CAGR of 14.2% through the cycle.

KSE-100 INDEX: Bulls in Control, Eyes on Next Leg (Technical Weekly)

Published August 11, 2025

The KSE-100 index maintained its bullish momentum, adding 4,347 points to close at 145,382 after hitting a weekly high of 146,813, extending the breakout above the 200% Fibonacci extension at 135,871 and now approaching the 261.8% level at 146,461. Price action continues to track the upper half of the rising channel, supported by both the 9-week and 30-week SMAs, reflecting strong underlying trend strength. However, the RSI has climbed to 79.76, deep in overbought territory, suggesting the risk of short-term profit-taking even as the broader uptrend remains intact.

KSE-100 INDEX: Channel Momentum Drives Bullish Continuation (Technical Weekly)

Published August 4, 2025

The KSE-100 index extended its winning streak, gaining 1,827 points to close the week at 141,035 after marking a high of 141,160. This reinforces the breakout above the 200% Fibonacci extension level at 135,871, with price action steadily climbing within the rising channel. The index remains well-supported above the 9- and 30-week SMA, indicating strong trend continuation. Meanwhile, the RSI has moved further into overbought territory at 77.35, reflecting robust momentum but also signaling the possibility of short-term cooling.

Economy: SBP maintains policy rate at 11%.

Published July 31, 2025

The State Bank of Pakistan (SBP) announced its monetary policy today (Wednesday), wherein the benchmark policy rate was kept unchanged at 11% for the second consecutive time.

Economy: Jul-25 NCPI expected at 2.9% YoY

Published July 29, 2025

The NCPI is expected to clock in at 2.9% YoY in Jul-25. On a monthly basis, the inflation in Jul-25 is projected to stand at 1.8% MoM. The base effect is melting away, signalling a comeback to a normalized inflation trend. The SBP estimates an inflation outlook in the range of 5-7% for FY26. Core inflation (NFNE) continues to remain sticky, with Jul-25 representing an increase of 7.8% YoY.

KSE-100 INDEX: Momentum Stays Strong, But Overheated (Technical Weekly)

Published July 28, 2025

The KSE-100 index extended its bullish momentum for the fifth consecutive week, adding 609 points to settle at 139,207 after briefly testing a high of 140,202. The index maintained its position above the key 200% Fibonacci extension level at 135,871, reinforcing the breakout achieved earlier. Price action remains well-aligned within the rising channel, with the next upside target visible near the 261.8% Fibonacci projection at 146,461. The RSI continues to hover in overbought territory around 76, suggesting strength, although stretched conditions may invite intermittent profit-taking.

KSE-100 INDEX: Bullish Momentum Persists, Resistance Test Ahead (Technical Weekly)

Published July 21, 2025

The KSE-100 index extended its bullish run for the fourth consecutive week, adding 4,297 points or 3.2% to close at 138,597 after marking a fresh high at 140,585. The index managed a decisive close above the 200% Fibonacci extension level of 135,871, drawn from the corrective move between the January 06 high of 118,735 and the May 05 low of 101,598. However, the price is now approaching the resistance trendline formed by connecting recent highs, suggesting the possibility of profit-taking in the near term, even as the broader momentum remains intact. The weekly RSI has climbed into overbought territory near 76 and broken its multi-month downward trendline, a sign of renewed strength. Trading volumes remain healthy, indicating active participation and continued buying interest.

KSE-100 INDEX: Upward Drive Tests Higher Extension Targets (Technical Weekly)

Published July 14, 2025

Building on last week’s strong breakout, the KSE-100 maintained its bullish momentum, closing at 134,299 with a further gain of 1.78% on steady volume. The index has surpassed the key 161.8% Fibonacci extension at 133,411 and is now eyeing the next upside target near the 200% extension around 137,500 (drawn from the recent corrective move from high of 126,718 to low at 115,887). The structure remains firmly aligned with the prevailing uptrend, holding comfortably above the 9- and 30-week moving averages, which reinforces confidence in continued strength. Positive price action and firm momentum suggest buying interest remains intact as long as the index sustains above the weekly gap near 132,130 left by the June 30 candle.

KSE-100 INDEX: Bullish Extension Eyes Next Breakout Zone (Technical Weekly)

Published July 7, 2025

The KSE-100 extended its bullish run last week, breaking decisively above the prior resistance with a strong close at 131,949, gaining 6% on higher volume of 1.42B. This move keeps the index firmly aligned with its long-term uptrend, testing the resistance line connecting recent tops. The weekly RSI has broken its descending trendline resistance, now at 71.58, confirming renewed momentum strength, though the index is nearing the wedge’s upper boundary, suggesting caution for possible profit-taking if overextension sets in.

KSE-100 INDEX: Bullish Engulfing Revives Uptrend Momentum (Technical Weekly)

Published June 30, 2025

Following two weeks of bearish pressure, the KSE-100 breached its long-term ascending bullish trendline but found solid footing around the 30-week SMA (115,615) aligning with the May 12 candle low at 115,794. This confluence zone acted as a strong support base, helping the index rebound sharply and close with a fresh weekly and daily high at 125,285, forming a bullish engulfing candle that effectively invalidates the immediate bearish bias. The weekly RSI also retested its descending trendline support and bounced back to 65.36, highlighting renewed momentum strength. Improved trading volume at 1.2B suggests fresh buying interest as the index respects the lower boundary of its long-term rising trendline.

KSE-100 INDEX: Downside Risks Mounting After Reversal Candle (Technical Weekly)

Published June 23, 2025

The confirmation of a gravestone doji followed by a bearish candle last week signals a potential reversal on the KSE-100 weekly chart. The index is currently testing critical horizontal support around 118,735, which aligns with both the long-term rising trendline and the 30-week SMA (118,895), making this confluence zone vital for the market’s near-term direction. A breakdown below this support may trigger a move toward the unfilled gap at 115,093 (left on May 12). Failure to hold this level could lead to a deeper correction toward the 50-week SMA (102,364), aligning with the December 2023 gap at 101,496.

Economy: SBP maintains policy rate at 11%

Published June 16, 2025

The State Bank of Pakistan (SBP) announced its monetary policy today (Monday), wherein the benchmark policy rate was kept unchanged at 11% aligning with market expectations.

KSE-100 INDEX: Island Reversal Threatens Uptrend Continuation (Technical Weekly)

Published June 16, 2025

The KSE-100 index tested the critical 127.2% Fibonacci extension (126,018), peaking at 126,718 before profit-taking dragged it down to 122,143. Despite a marginal weekly gain of +0.41%, the index formed a bearish shooting star on June 12, followed by a gap-down on June 13, offsetting the earlier June 10 gap-up. This sequence forms an Island Reversal pattern, a bearish signal, unless invalidated by a sustained move above the June 13 gap at 123,847. Reclaiming this level and then 126,718 would shift bias back in favor of bulls.

Economy: MPC likely to keep the policy rate unchanged

Published June 13, 2025

The State Bank of Pakistan’s (SBP) Monetary Policy Committee (MPC) is scheduled to convene on June 16, 2025. We expect the MPC to take a cautious stance and maintain the policy rate at 11%. Given the cumulative 11 percentage points reduction over the past 12 months, the SBP may opt to pause its rate-cutting cycle in the upcoming meeting. Our expectation is underpinned by several key factors, including re-basing of energy prices due at fiscal year-end, rising geopolitical tensions in the Middle East, and potential pressure on the PKR. These factors may influence the SBP to take a cautious stance and defer the rate cut until more clarity emerges.

Federal Budget FY26: Reforming Where It Hurts

Published June 11, 2025

The Federal Budget for FY26 aims to address the IMF’s longstanding demands by targeting the informal economy, streamlining the size of the government, and phasing out subsidies and tax exemptions. Furthermore, fiscal numbers not only look believable but also achievable. Growth target, however, seems a bit ambitious. The budget not only restricts undocumented individuals from acquiring assets, but also seeks to disrupt their business activities by limiting the ability of registered taxpayers to claim deductions on purchases made from non-filers. The budget prioritizes real direct investment by maintaining capital gains and dividend tax rates on equities, while increasing taxes on profit from debt instruments and dividends from mutual funds. Remaining cognizant of the middle class’s declining purchasing power, the budget rationalizes income tax on salaried individuals to support disposable income and economic growth. Given the formal sector’s pivotal role in driving equity market flows, this measure is likely to have a materially positive impact on the stock market.

KSE-100 INDEX: Bullish Signal Strengthens After Consolidation (Technical Weekly)

Published June 10, 2025

The KSE-100 index closed the week at 121,641, gaining 1.63% and posting a strong bullish candle that confirmed a breakout above the multi-week resistance zone of 120,797. This move, supported by sustained positioning above the 9-week (116,556) and 30-week (113,194) moving averages, reinforces the prevailing uptrend and opens room for further upside toward the 126,018 (127.2% Fibonacci extension) and potentially 132,660 (161.8%) levels align with trendline resistance. Importantly, the RSI has broken above its descending trendline, confirming a bullish momentum shift that supports the breakout.

KSE-100 INDEX: Indecision Near Highs, Trend Intact (Technical Weekly)

Published June 2, 2025

The KSE-100 index closed the week at 119,691, posting a modest gain of 0.49% and forming a small-bodied candle with upper and lower shadows, reflecting indecision around the recent highs. Encouragingly, the index continues to hold above the 9-week SMA (116,240), reinforcing the short-term bullish structure. The support zone between 115,093 and 115,790 has held for three consecutive weeks, validating its significance. Notably, weekly volumes surged to 1.2 bn shares from 831 million last week, reflecting renewed participation.

KSE-100 INDEX: Uptrend Holds, Breakout Awaits (Technical Weekly)

Published May 26, 2025

The KSE-100 index closed the week slightly lower at 119,102, losing 0.46% after testing 120,699 but failing to surpass April’s high of 120,797. The formation of an upper wick signals profit-taking near resistance. Despite the mild pullback, the index remains above its 9-week SMA (116,030) and the key support zone between 115,093 and 115,790, which held firm during last week’s retracement, preserving the short-term bullish bias.

KSE-100 INDEX: Rally Gains Steam Amid Caution Signals (Technical Weekly)

Published May 19, 2025

The KSE-100 index rebounded sharply this week, gaining 11.64% to close at 119,649, reclaiming key broken supports and signaling a potential return to bullish momentum. The rally began with a gap-up opening, now forming critical support between 115,093 and 115,790, marked the highest weekly close on record. Notably, this move was accompanied by the highest volume seen over any five-week period in the current rally, indicating renewed institutional interest. The April peak at 120,797 remains immediate resistance, and a sustained breakout above it could open the path toward the 127.2% Fibonacci extension of the recent corrective move from 120,797 to 101,597 at 126,000, with further upside potential toward the trendline around 130,000.

KSE-100 INDEX: Cautious Rebound within a Weakening Trend (Technical Weekly)

Published May 12, 2025

The KSE-100 index suffered a steep weekly decline of 6.08%, closing at 107,174 and firmly breaking below the key support cluster around 109,859. This breakdown not only violated the horizontal range support but also pierced the long-standing trendline and the 30-week SMA (109,171), confirming a shift in structure from range bound to corrective. The index also filled the previously highlighted gap at 101,496, which now becomes a reference level for potential stabilization in the coming sessions. The weekly RSI dropped sharply to 43.56, the lowest since August 2023, reinforcing the loss of bullish momentum and signaling a shift toward a bearish regime.

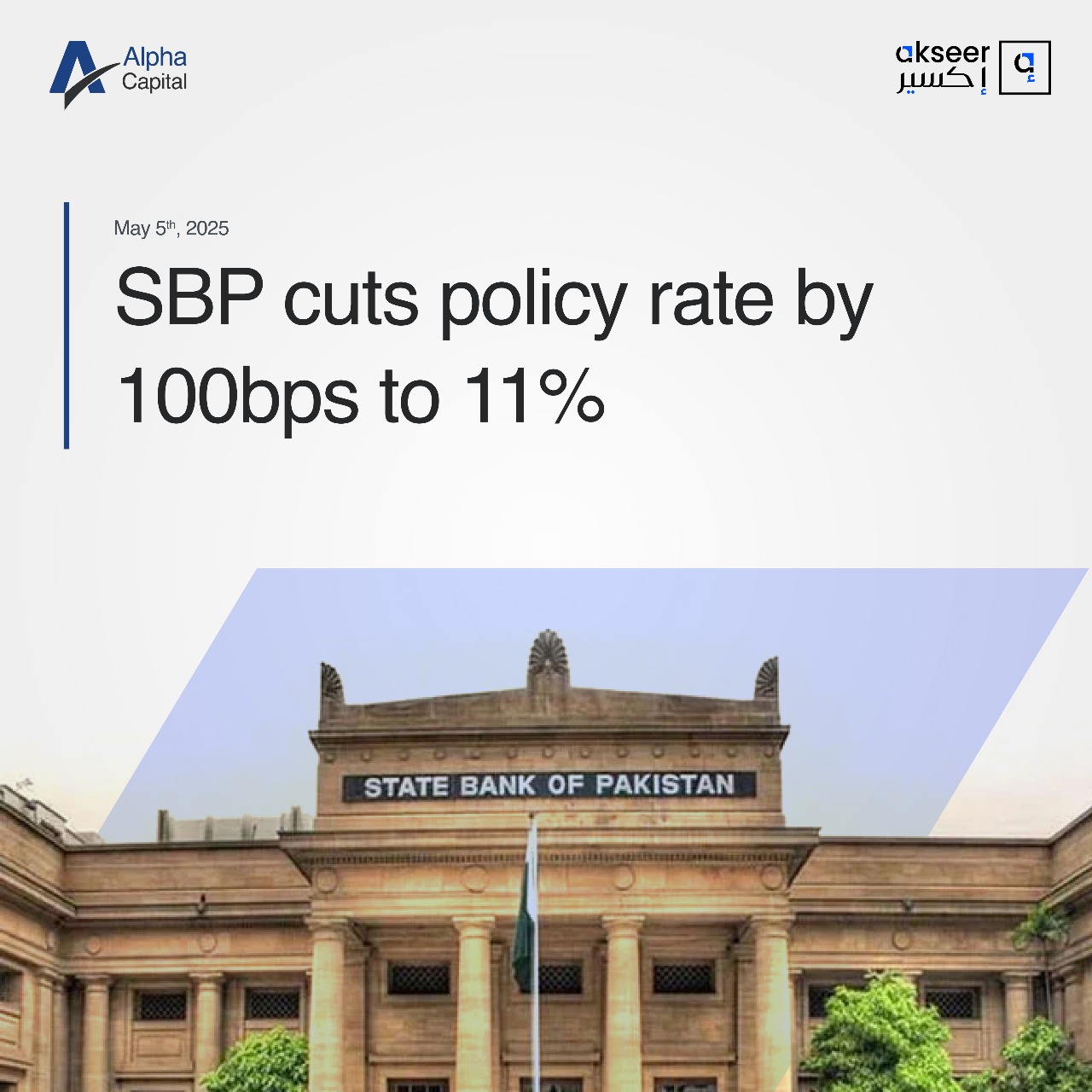

Economy: SBP slashes policy rate by 100bps to 11%

Published May 6, 2025

The State Bank of Pakistan (SBP) announced its monetary policy today (Monday), wherein the policy rate was cut by 100bps to 11%. This latest move brings the cumulative rate cuts to 1,100bps since Jun-24.

KSE-100 INDEX: Support Cluster Holds, but Momentum Weakens (Technical Weekly)

Published May 5, 2025

The KSE-100 index witnessed another highly volatile week, falling 1.17% to close at 114,114. During the session, it tested a weekly low of 110,632, aligning closely with a major support cluster comprising the long-term trendline, the horizontal support at 109,859, and the 30-week SMA (108,448). This confluence of supports helped the index trim early losses. The broader structure remains range bound between 120,797 and 109,859, a horizontal channel that has persisted since mid-December. A decisive breakout from this range is required to establish the next directional trend. The weekly RSI declined further to 59.80 from 62.74, marking a new low and staying below the August support-turned-resistance at 66.69. This continued slide reflects weakening momentum and suggests caution heading forward.

Economy: MPC likely to cut policy rate by 50bps

Published May 2, 2025

We anticipate the State Bank of Pakistan (SBP) to reduce the policy rate by 50bps in the upcoming MPC meeting on May 5th, 2025. The revised policy rate would settle at 11.5%. Our expectation is primarily driven by favorable economic factors, namely i) an improvement in external account, ii) a decline in headline inflation, and iii) falling global commodity prices. The geopolitical situation still remains fluid, with rising tensions on the eastern border alongside US-China trade war. These factors may influence the SBP to take a cautious stance and defer the rate cut until more clarity emerges.

OCTOPUS: Bullish Setup Forms Near Long-Term Trendline (Flash Note | Pakistan Technicals)

Published April 30, 2025

Octopus (LDCP 50.48) has confirmed a potential double-bottom formation today by closing above the key support level of 49.00. This rebound follows a prolonged downtrend from the August 2023 high of 121.35 to a low of 49.00, which was first tested on April 09. The pattern is developing near a long-term ascending trendline, adding further significance to this support zone. The daily RSI has formed a higher low at 35.70 versus 24.90 on April 09, while price retested the 49.00 level, confirming a bullish divergence and signaling weakening selling momentum.

KSE-100 INDEX: Momentum Fades as Range-bound Action Persists (Technical Weekly)

Published April 28, 2025

The KSE-100 index extended its consolidation phase last week, shedding 1.57% to settle at 115,469. After filling the gap between 117,600 and 118,790, left from April 7 on the daily chart, the index faced rejection and reversed lower. This pullback tested the 100-day SMA around 113,790, where initial buying support emerged. The broader structure remains range-bound between 120,797 and 109,859, with the trend still classified as sideways within this horizontal channel. The weekly RSI retested and faced rejection at the August support-turned-resistance near 66.69, sliding to a fresh low at 62.74 and confirming bearish momentum ahead.

Economy: Apr-25 NCPI expected at 0.2% YoY

Published April 25, 2025

The headline CPI is expected to ease further in Apr-25, clocking in at 0.2% YoY, continuing the declining inflation trend. This represents the lowest inflation reading for the past six decades, largely attributable to notable reductions in food and housing segments amid lower electricity prices and post-Ramzan factor. Moderate demand and stable PKR/USD parity have kept price levels moderate since the beginning of 2024, with a cumulative price increase of a mere 3.3% since Dec’23. Average inflation during 10MFY25 is now expected to settle at 4.8%, significantly lower than 26.2% recorded in the same period last year (10MFY24).

KSE-100 INDEX: Price Recovers, Yet Uptrend Awaits Validation (Technical Weekly)

Published April 21, 2025

The KSE-100 index rebounded sharply last week, posting a 2.14% gain to close at 117,315, as buyers stepped in near the lower boundary of the ongoing consolidation range. Despite the recovery, the index remains confined within the broad horizontal structure that has persisted since December, with boundaries at 118,790 and 109,859. The weekly RSI has recovered to 66.91 after briefly slipping below its August support at 66.69 suggesting a potential retest of the broken support zone, though a follow-through move is required to confirm directional strength.

KSE-100 INDEX: Rising Risks After RSI Breakdown (Technical Weekly)

Published April 14, 2025